Vested App Review: Is This the Best App to Invest in US Stocks From India?

Vested focuses exclusively on US stocks and ETFs for India-based investors: fractional shares, pre-built “Vests”, and a lighter interface compared to all-in-one apps. It suits passive-to-moderate investors who want US exposure rather than frequent trading—compare charges, withdrawal timelines, and KYC steps on the official Vested site before funding.

However, you still need to understand:

- The true cost of investing (forex, transfer and withdrawal fees).

- The regulatory structure (Vested partners with US brokers like DriveWealth, rather than being a US broker itself).

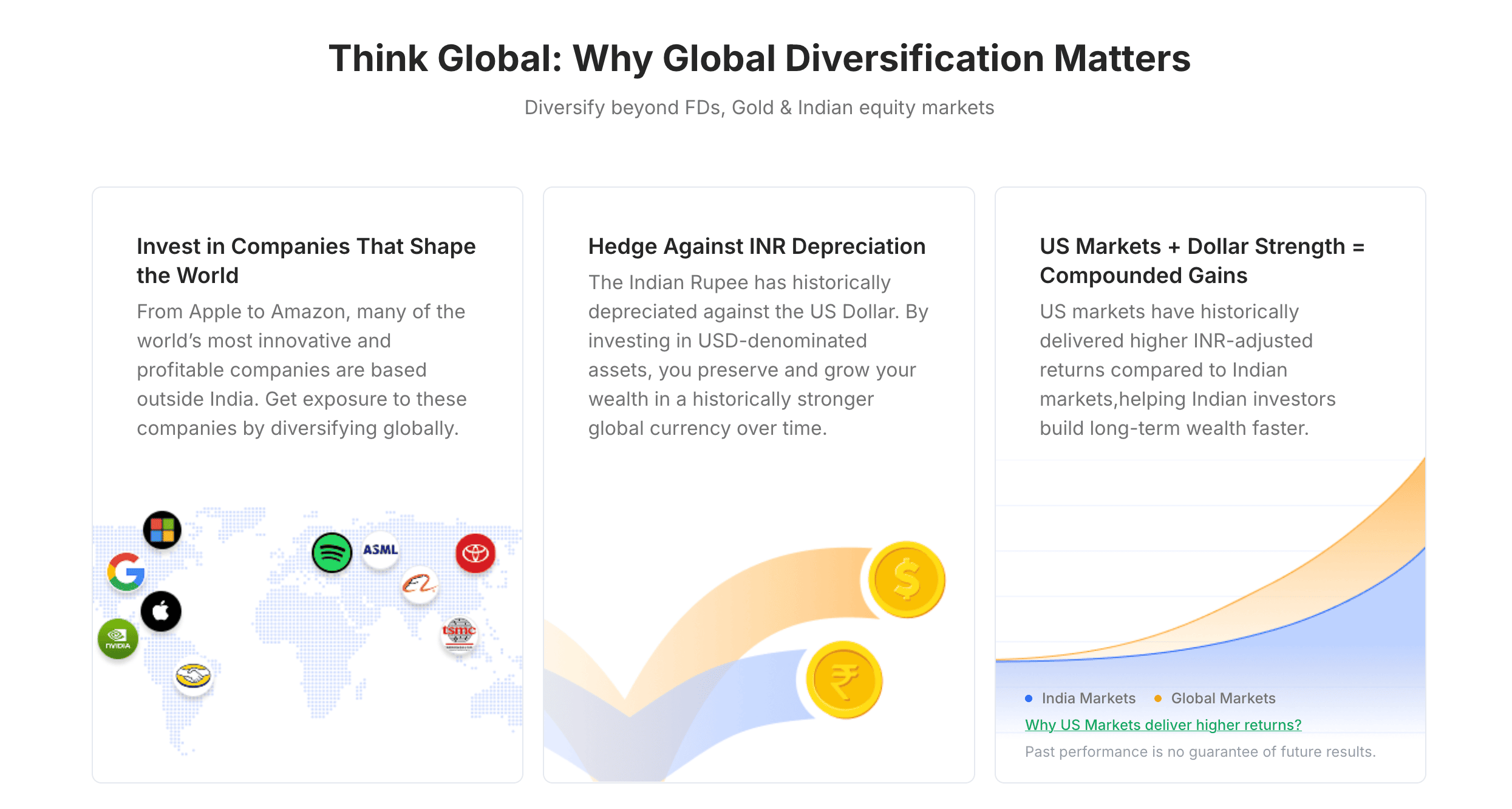

- The limitations of a US‑only app versus an “all‑in‑one” platform like INDmoney.

This review will help you decide if Vested fits your profile or if you’re better off with other routes to invest in US markets.

Table of Contents

What Is Vested?

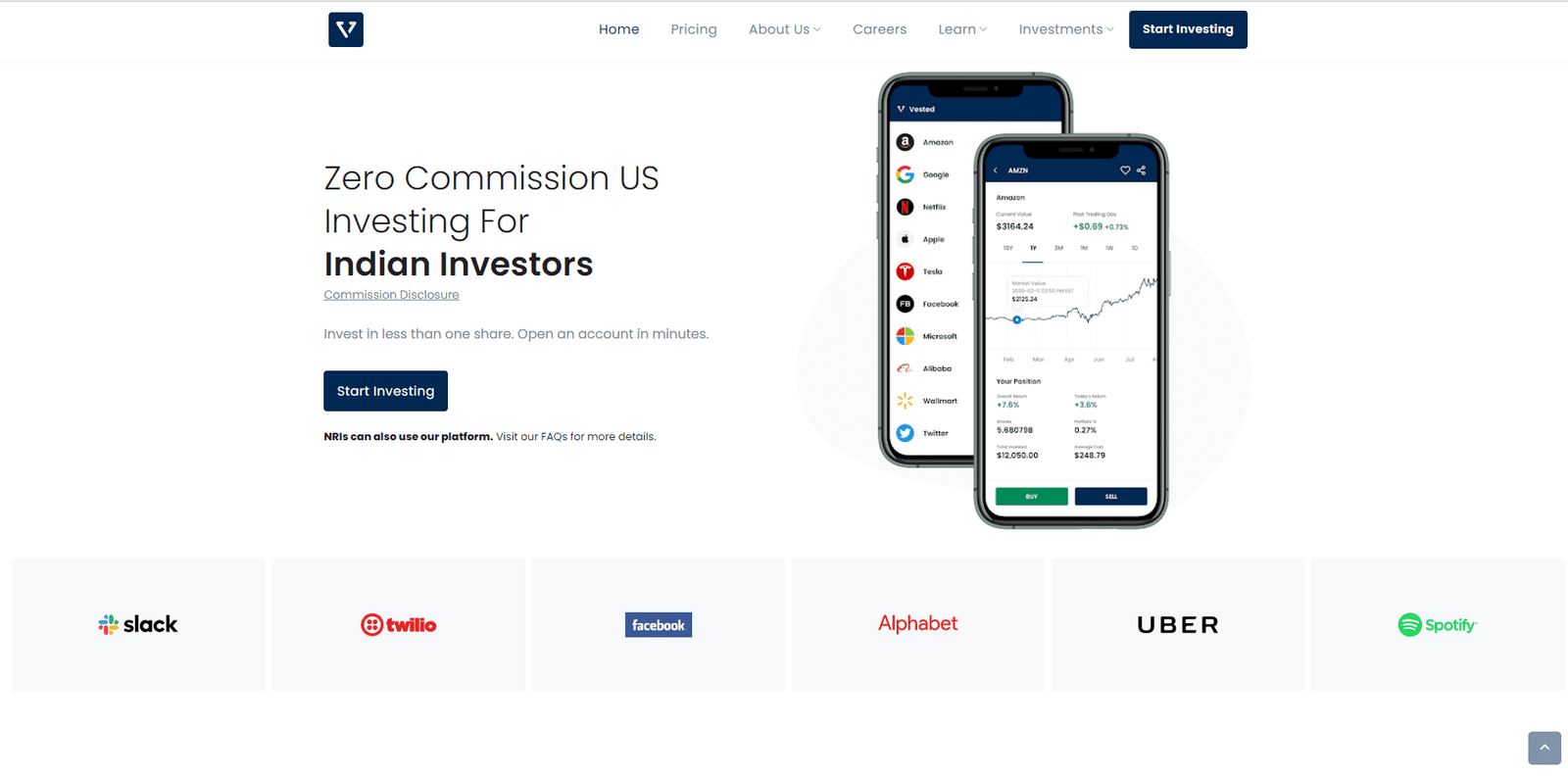

Vested is a digital investment platform that lets Indian investors invest in US stocks and ETFs through a mobile app and web interface. It aims to simplify global investing by taking care of onboarding, compliance with RBI’s Liberalised Remittance Scheme (LRS) flows (where applicable), and connecting you to a regulated US broker.

Instead of opening an account directly with a foreign broker, you sign up with Vested. Behind the scenes, your US brokerage account is usually opened with their partner (DriveWealth), and Vested provides the front‑end interface and India‑specific support.

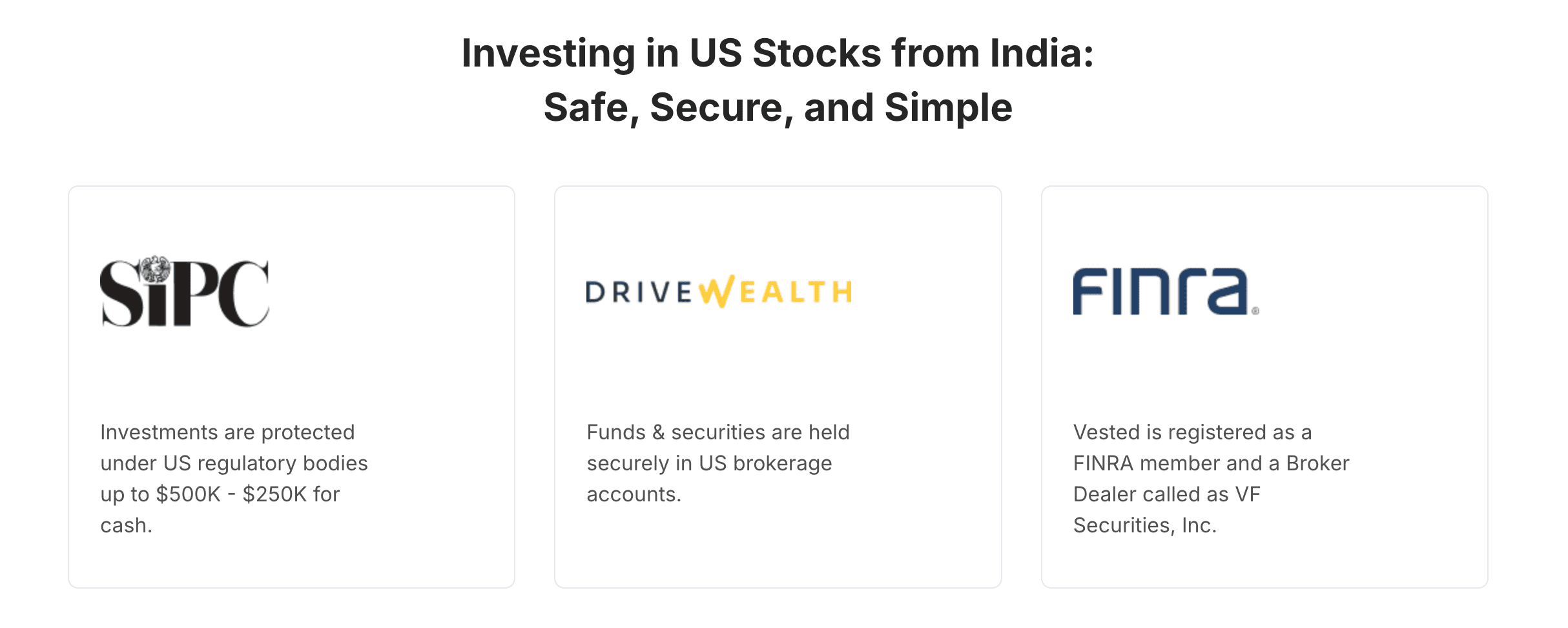

Is Vested Safe and Legit?

Regulatory Framework

Vested itself is not a US stock exchange or custodian; it’s a platform that partners with regulated entities such as DriveWealth in the US. The key safety points to understand:

- Your US securities are typically held with the US custodian / partner broker, not directly with Vested.

- DriveWealth and similar partners are regulated in the US; check their current regulatory status and protections (for example, SIPC‑like protections for the brokerage).

- In India, Vested positions itself as a facilitator for overseas investing, working within RBI and SEBI compliance frameworks.

Always verify the latest regulatory details on Vested’s official website and disclosures before moving large amounts.

Data & App Security

From a user’s perspective, safety also means how your data and logins are handled:

- Vested uses typical fintech security measures like encryption and secure sign‑in.

- Enable any available 2FA / OTP‑based security features in the app.

- Avoid using unsecured public Wi‑Fi when logging in or funding your account.

Reputation and User Feedback

On the Apple App Store, “Vested: US Stocks Investing” generally has a strong rating (around 4.6/5 across thousands of reviews), which suggests the app experience is solid for most users, though not perfect. Some reviews highlight smooth onboarding and good support, while others mention occasional bugs or slow performance during peak times — common issues across most investing apps.

Key Features of the Vested App

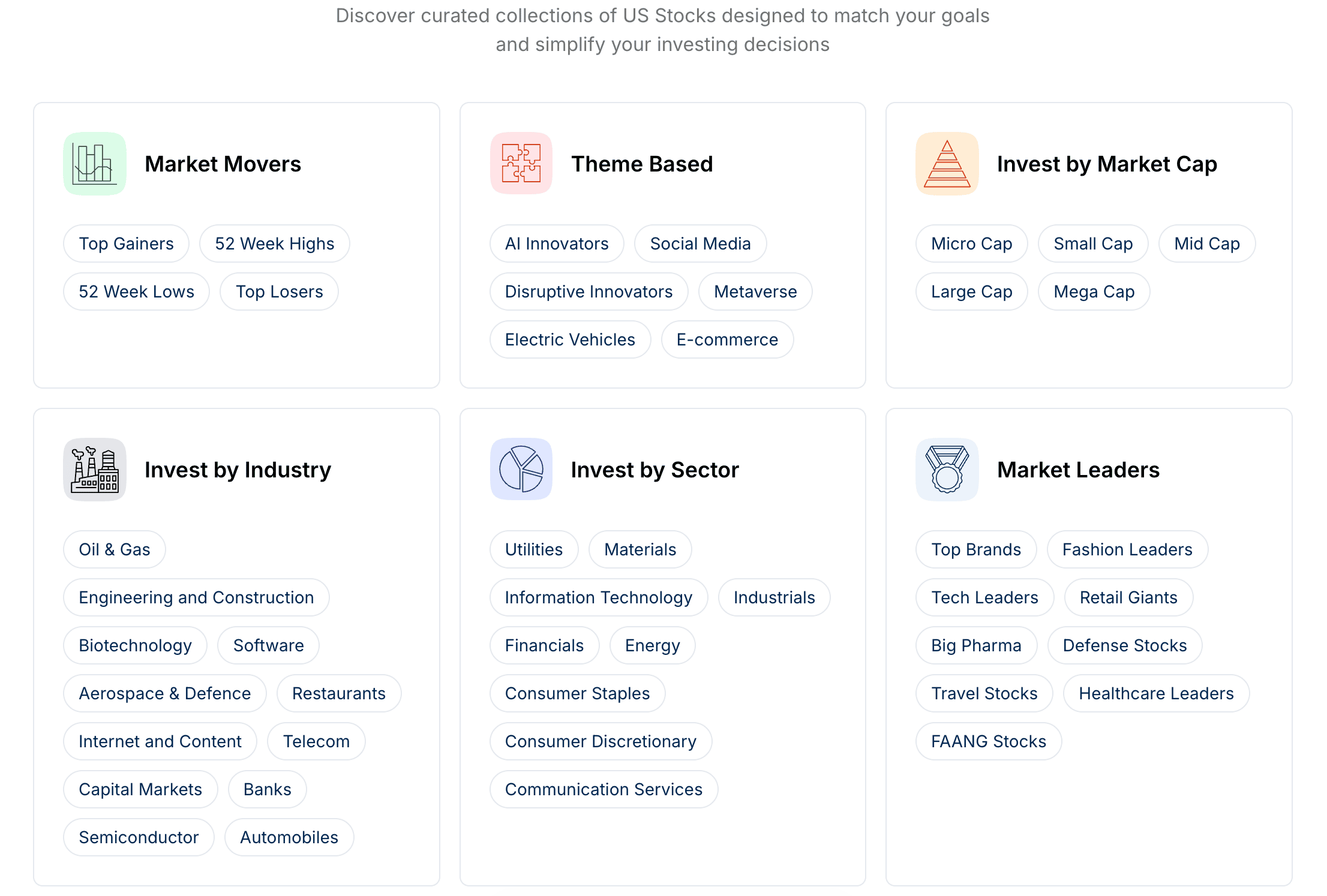

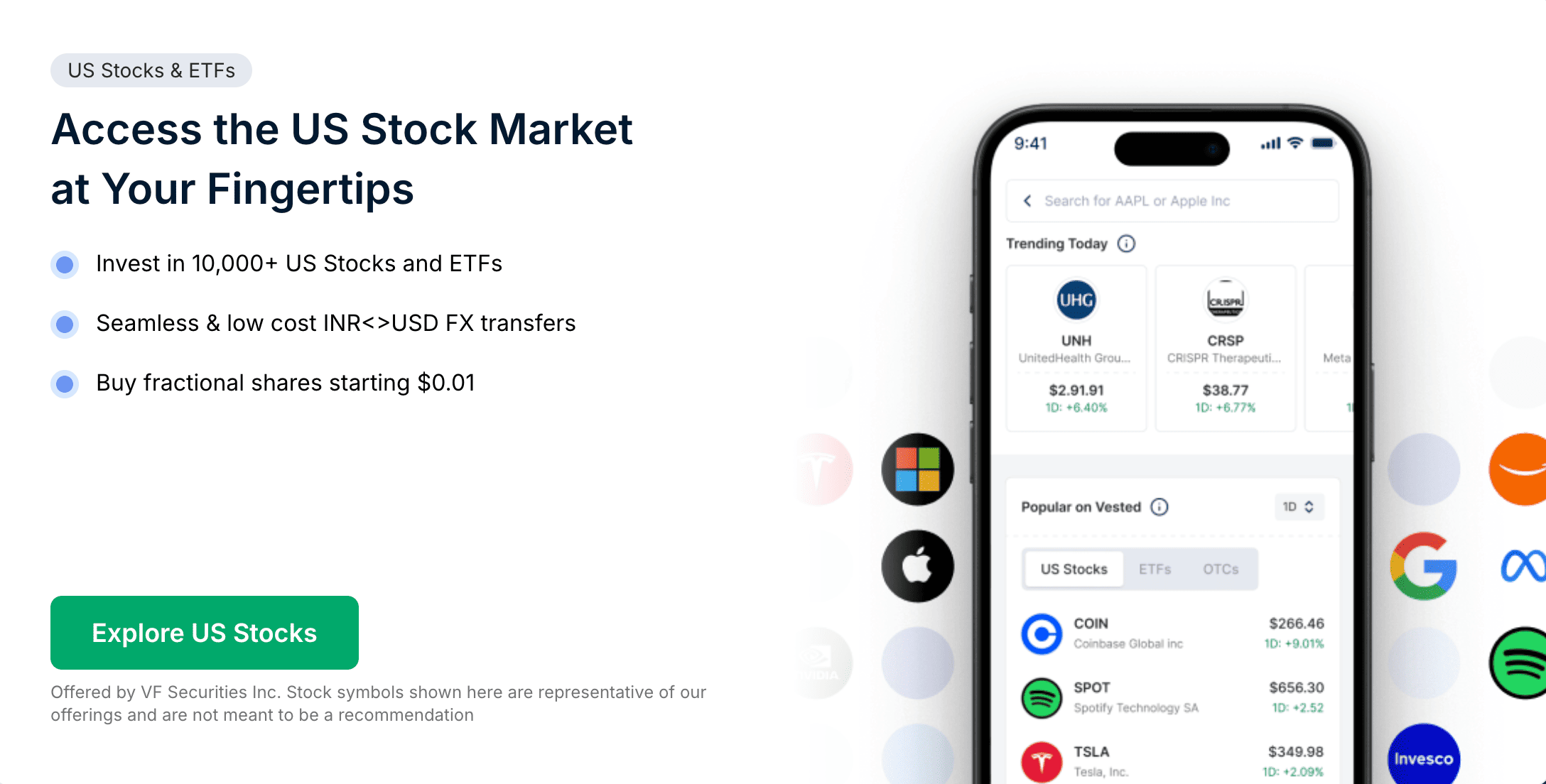

US Stock and ETF Access

Vested offers access to 1,500+ US equities and ETFs, giving Indian investors exposure to major companies and index funds. This includes blue‑chip names, growth stocks, sector ETFs, and thematic funds.

You get:

- Real‑time quotes and basic charts.

- The ability to buy individual stocks and diversified ETFs.

- Both lump‑sum and systematic (recurring) investing options.

Fractional Investing

US stocks can be expensive per share. Vested’s fractional investing lets you buy portions of a share (for example, investing 50 USD into a 300‑USD stock). This is helpful if you are starting with smaller ticket sizes but still want exposure to specific companies or ETFs.

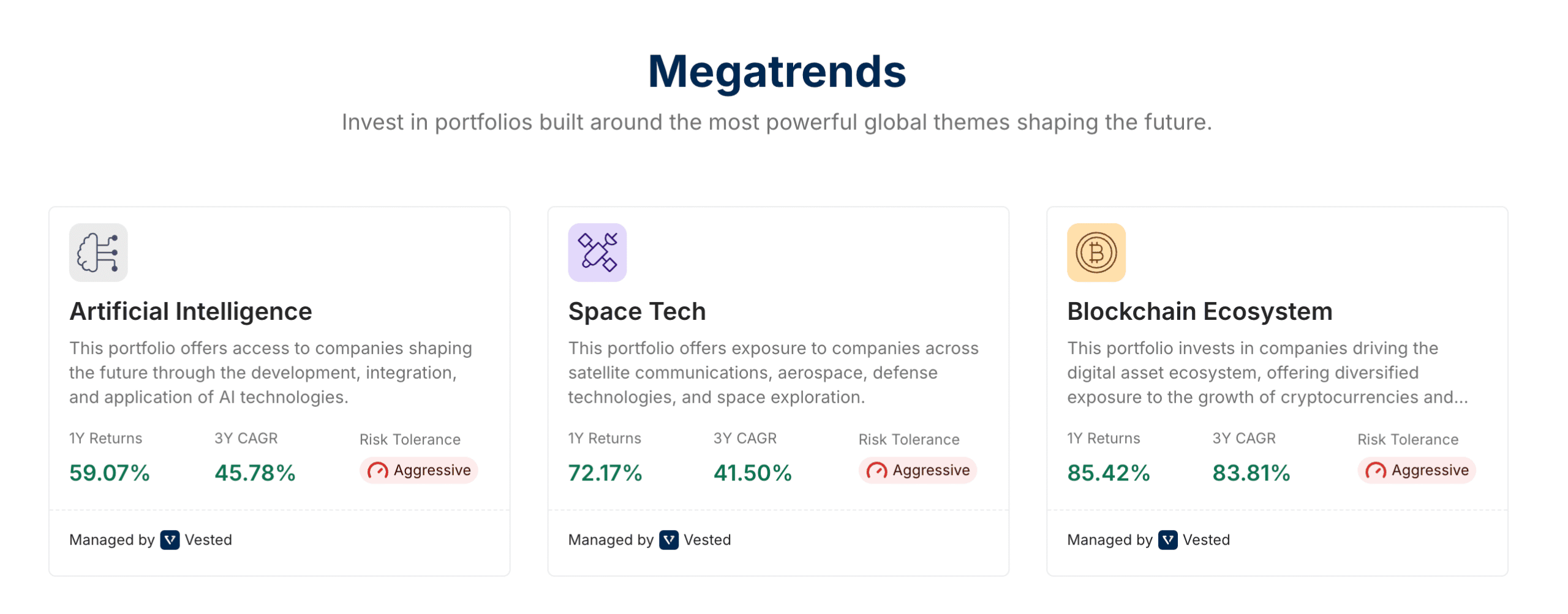

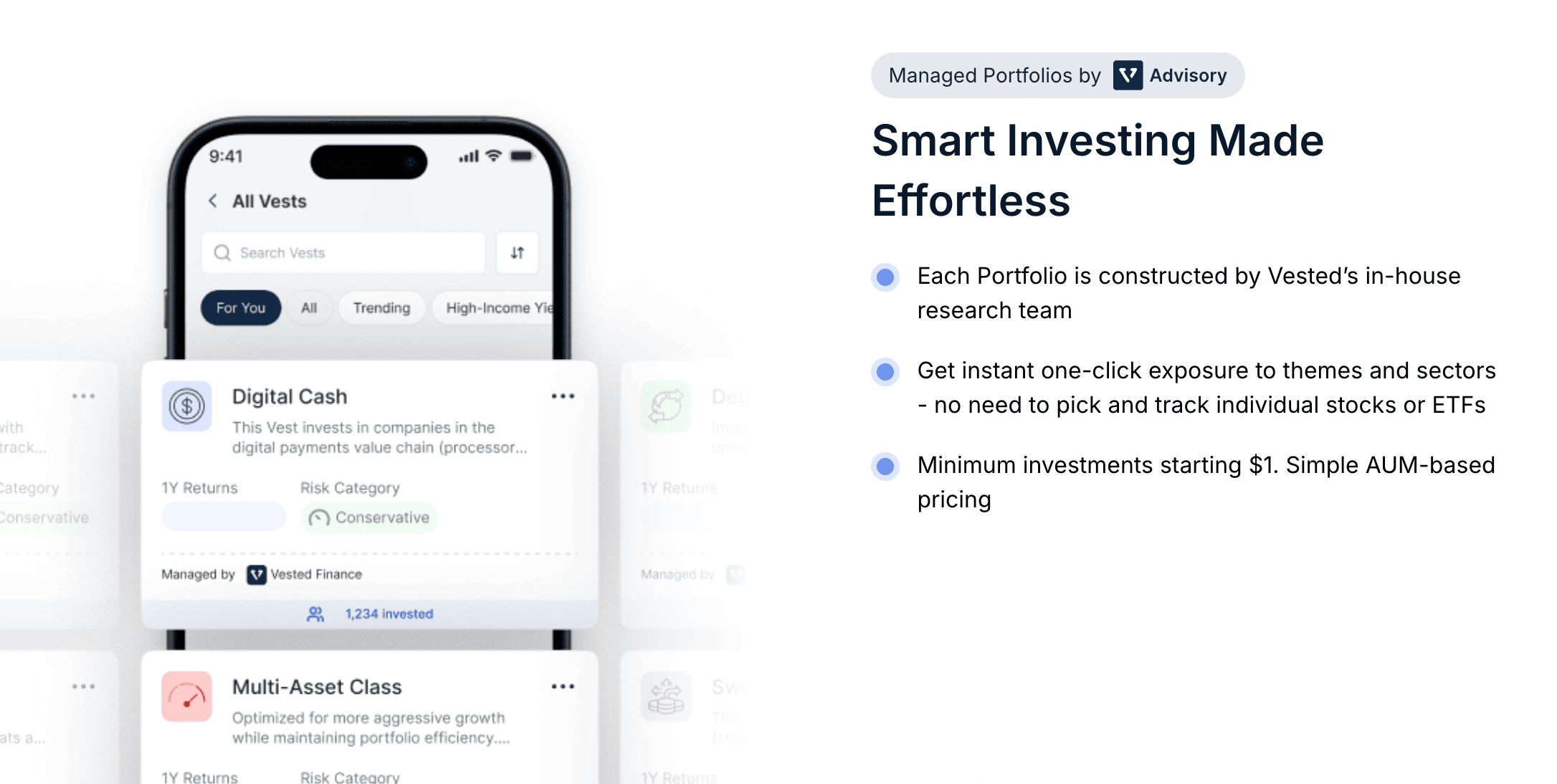

Pre‑Built Portfolios (“Vests”)

Vested offers curated portfolios called “Vests”, which bundle multiple US securities around a theme or strategy: for example, technology, dividend stocks, or broad‑market ETFs.

These are useful if:

- You don’t want to pick individual stocks.

- You prefer a packaged strategy, such as a low‑cost, broad‑market exposure.

Still read the underlying holdings, expense ratios, and historical volatility of each Vest before investing.

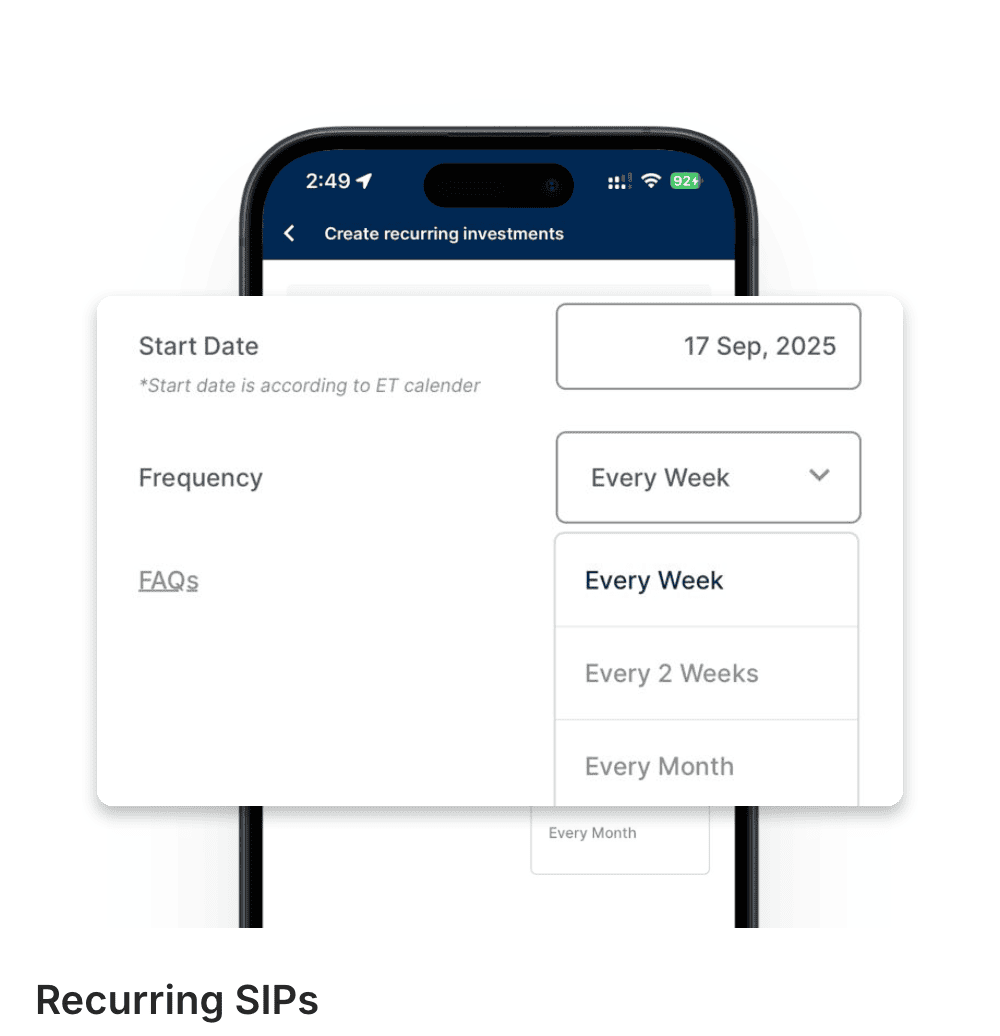

Recurring Investments (SIP‑Style)

For long‑term wealth building, Vested allows recurring investments (similar to SIPs), where you automatically invest a fixed amount periodically into chosen stocks, ETFs, or Vests. This can help you benefit from dollar‑cost averaging and build a disciplined habit.

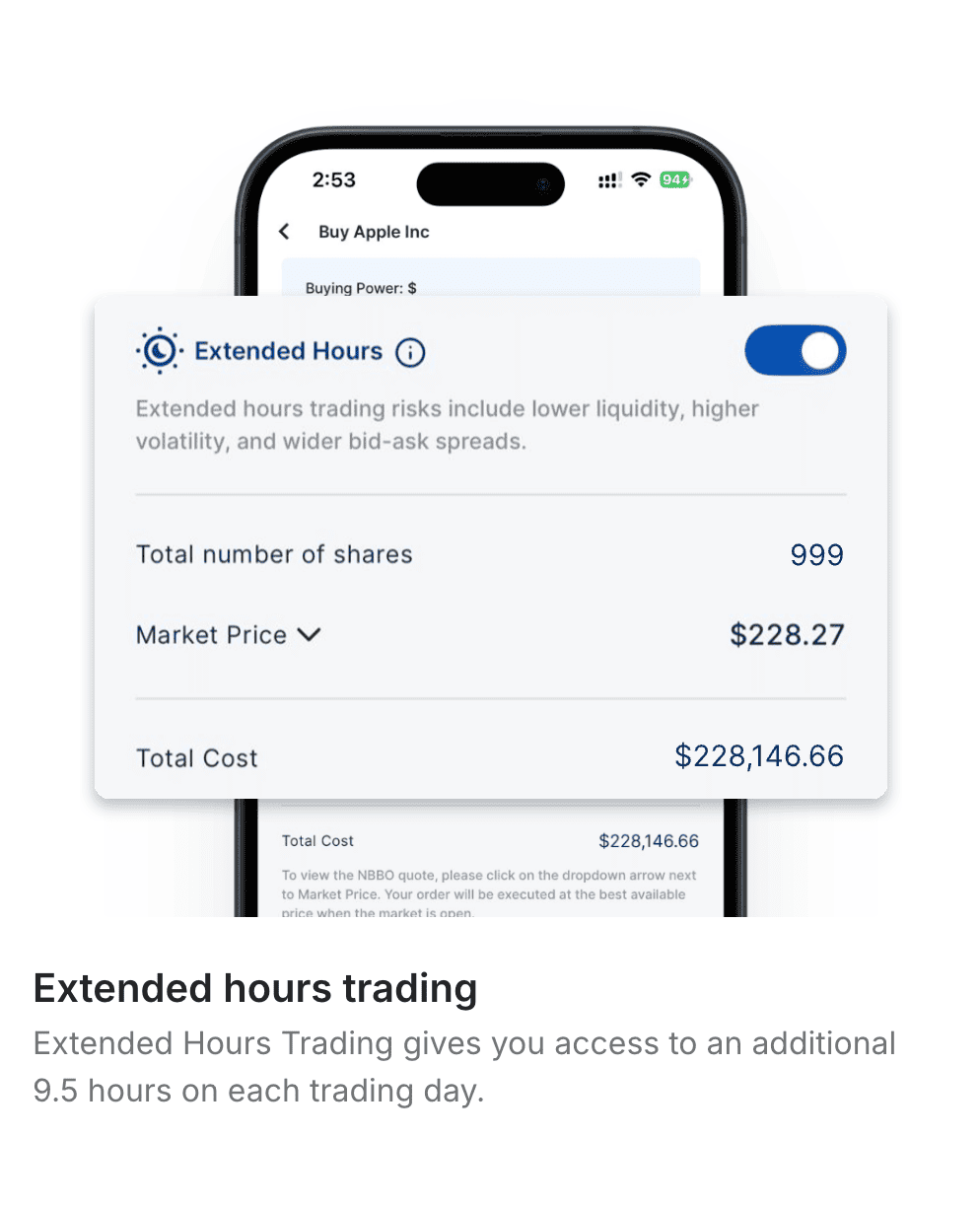

Extended‑Hours Trading & Other Tools

Vested may provide access to certain extended trading hours and additional tools, depending on your account type and partner broker setup. Check in‑app for the latest feature list — these advanced tools mostly matter if you are not just a passive long‑term investor.

Vested Charges and Fees (What Really Matters)

Marketing phrases like “zero‑commission trading” are attractive, but you must understand the full fee stack.

1. Brokerage / Trading Commissions

Vested promotes zero‑commission trading on US stocks and ETFs in many cases, which means you don’t pay a per‑trade brokerage fee for standard trades. However:

- Certain securities (like OTC securities or specific instruments) can have separate fees or a percentage‑based charge.

- If you use advanced or premium features, there may be subscription or membership fees.

Always read the current pricing page; fee structures can evolve.

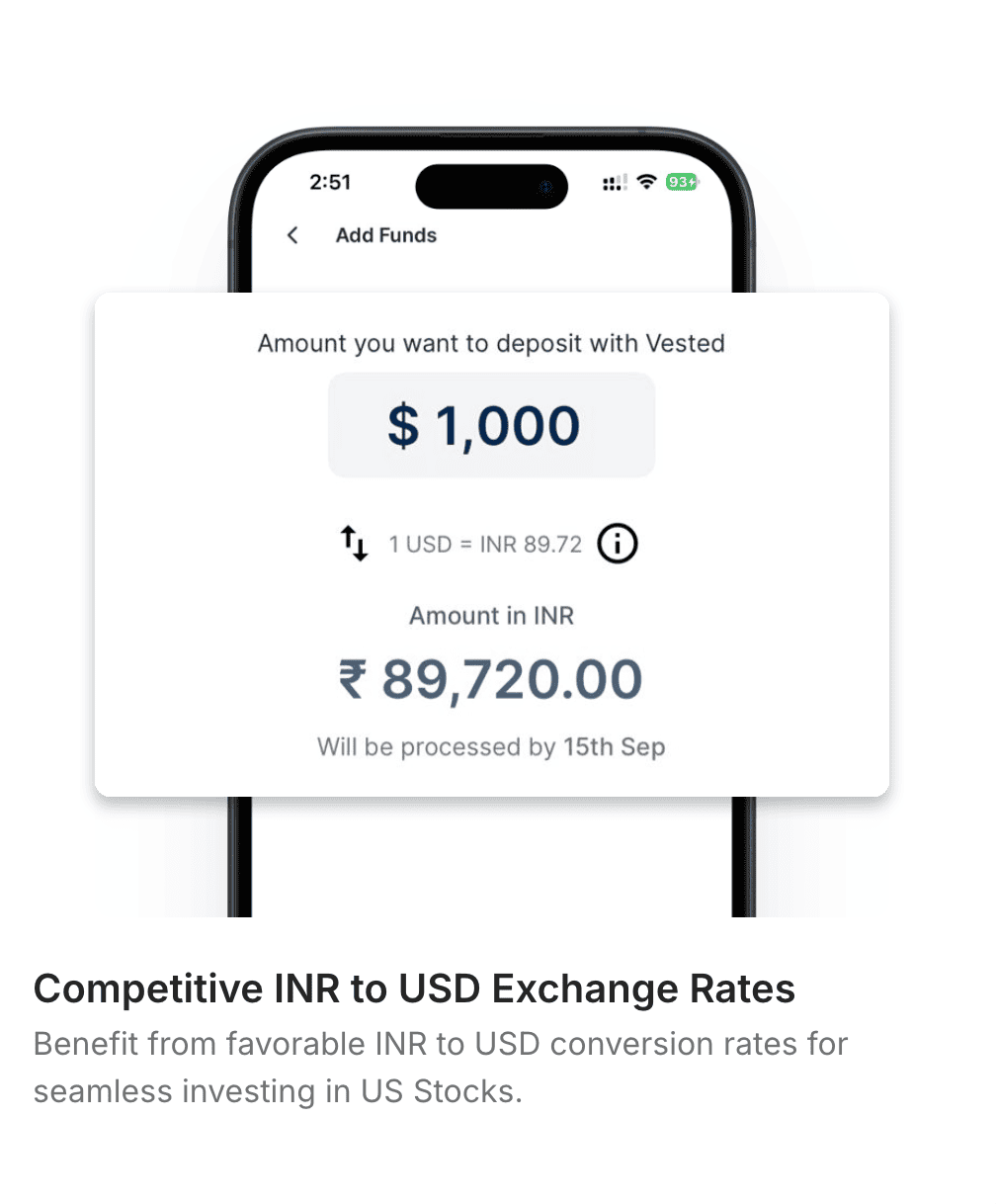

2. Forex and Funding Costs

When you fund your US account, money has to move from INR to USD. Costs can include:

- Forex markup by the bank or payment partner.

- Fixed bank charges for outward remittances (varies by bank).

Vested also highlights “zero fixed fees on USD deposits with Vested Direct” and “zero‑commission trading” as part of certain offers, but forex conversion costs may still apply depending on the route and banking partner. Do not assume that “zero fixed fees” equals “zero total cost.”

3. Withdrawal Fees

When you withdraw money from the US account back to India, there may be:

- A fixed withdrawal fee per transaction (for example, around 5 USD per withdrawal in some setups).

- Bank charges and conversion back to INR.

To keep costs low, avoid frequent small withdrawals; plan fewer, larger withdrawals instead.

4. Other Charges

Also account for:

- Possible platform or subscription fees for premium offerings.

- Any fees embedded in specific Vests or managed portfolios.

- US withholding tax on dividends and Indian capital gains tax on profits.

Always cross‑check the latest fee structure on Vested’s official site and compare it to other platforms like INDmoney.

Vested vs INDmoney vs Other US‑Stock Apps

Vested

- Specialised US‑only platform.

- 1,500+ US stocks and ETFs; strong fractional investing focus.

- Pre‑built Vests and SIP‑style recurring investments.

- Good if you want a dedicated US investing app.

INDmoney

- All‑in‑one wealth app with US stocks, Indian mutual funds, Indian stocks, fixed income, and more.

- Strong portfolio tracking and goal‑based investing tools.

- Better if you want to manage India + US in one dashboard and like consolidated reporting.

Other Routes

International mutual funds/ETFs via Indian brokers are good for people who want simple, rupee‑denominated US exposure without dealing with foreign accounts.

GIFT City platforms and direct international brokers can be suitable for advanced users who want broader global access and are comfortable with more complex documentation.

Who Should (and Shouldn’t) Use Vested?

Vested Is a Good Fit If You:

- Specifically want to build a US equity allocation in your portfolio.

- Appreciate a clean, focused interface rather than a noisy all‑in‑one super‑app.

- Are willing to learn about LRS, forex costs, and tax implications.

- Prefer curated themes (Vests) or ETF‑based portfolios over random stock picking.

Vested May Not Be Ideal If You:

- Want a single app for Indian stocks, mutual funds, and US stocks together.

- Trade aggressively in intraday or derivatives — Vested is more for long‑term US investing than for F&O style trading.

- Don’t want to deal with cross‑border tax and reporting at all (in which case international mutual funds or global ETFs listed in India may be simpler).

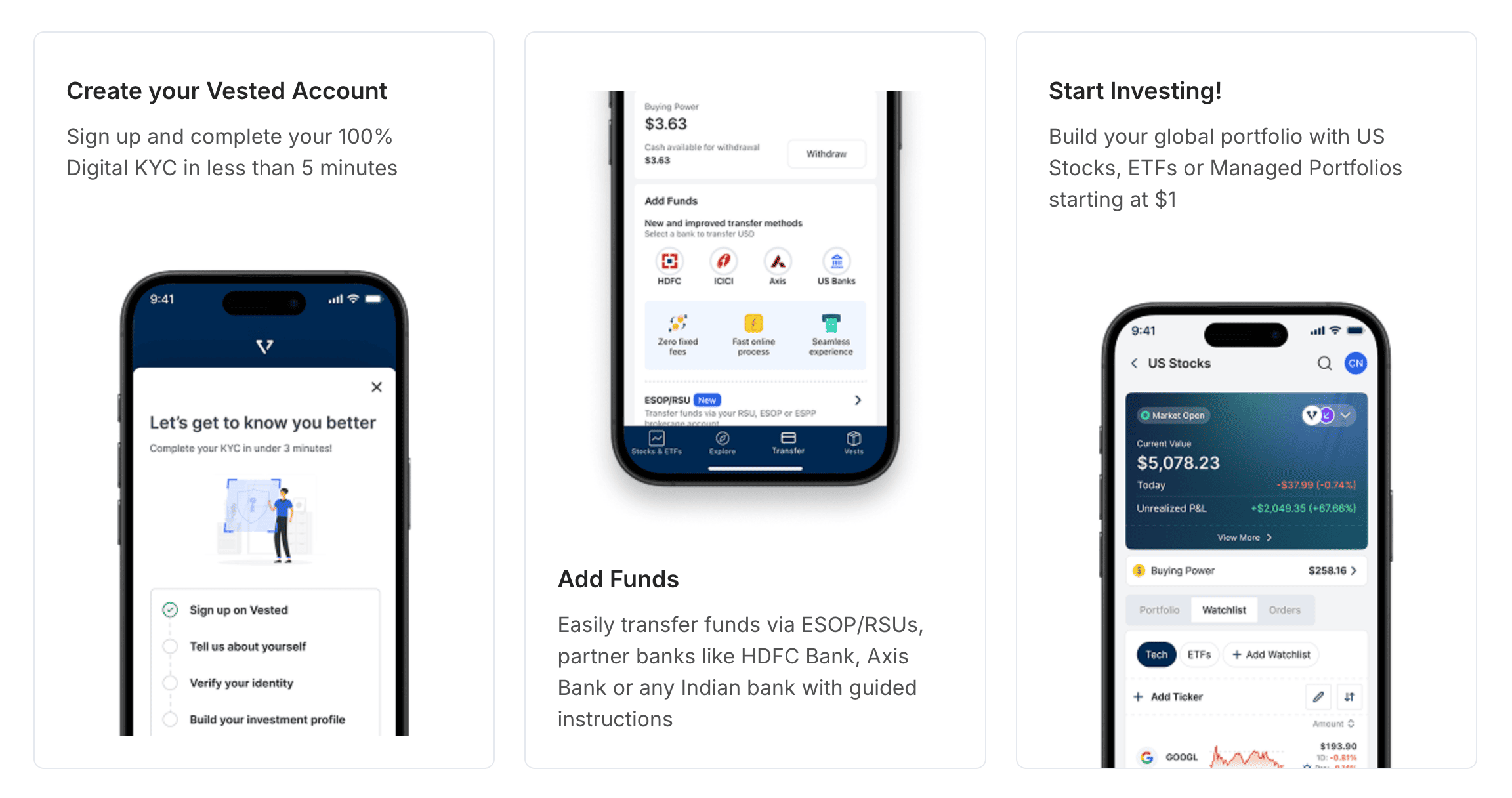

Step‑by‑Step: How to Open and Use Vested

- Download the Vested app from the Play Store or App Store, or visit the web platform.

- Sign up and complete KYC by providing PAN, identity documents, and basic information.

- Open your US brokerage account within Vested; this typically happens via their partner (like DriveWealth).

- Fund your account using the available options (Vested Direct / bank transfer, etc.), keeping LRS limits and bank charges in mind.

- Choose what to invest in: individual stocks, ETFs, or Vests.

- Set up recurring investments if you want a SIP‑like schedule.

- Monitor and rebalance periodically based on your goals and risk tolerance.

- Plan withdrawals thoughtfully to minimise fixed withdrawal charges and forex slippage.

Vested Pros and Cons (Summary)

Pros

- Access to a wide range of US stocks and ETFs with fractional investing.

- Pre‑built portfolios (Vests) for theme‑based or diversified exposure.

- Zero‑commission trading on many US securities, subject to terms.

- SIP‑style recurring investments to average out entry price.

- Focused US‑only app, which keeps the interface relatively clean.

Cons

Some user feedback mentions occasional performance issues or onboarding friction, like many investing apps.

US‑only; not a one‑stop solution for your entire portfolio.

Forex, funding, and withdrawal costs can still be significant.

Tax and regulatory complexity (double‑country considerations).

Some user feedback mentions occasional performance issues or onboarding friction, like many investing apps.

Also read: 5Paisa vs Upstox

Final Thoughts: Should You Use Vested?

Vested is a credible, focused way for Indian investors to access US stocks and ETFs, especially if you value fractional investing, curated portfolios, and a simple interface. It’s not a magic shortcut — you still need to understand risks, costs, and tax implications.

If you:

- Want to add US exposure to a diversified portfolio, and

- Are okay managing a separate US account and cross‑border compliance,

then Vested can be a useful tool in your investing toolkit.

If you want everything under one roof or don’t want to deal with cross‑border complexity at all, look at alternatives like INDmoney or India‑listed international mutual funds and ETFs.